MEMBER'S LOGINX

| Invalid Username / Password | ||||||||

| Invalid Captcha | ||||||||

|

||||||||

| Sign Up | Forgot Password? | ||||||||

- Home

- Views On News

- Oct 25, 2023 - Top 5 Undervalued Smallcap Stocks to Watch Out for in 2024

Top 5 Undervalued Smallcap Stocks to Watch Out for in 2024

The mainstream media all over is talking about yesterday's market correction.

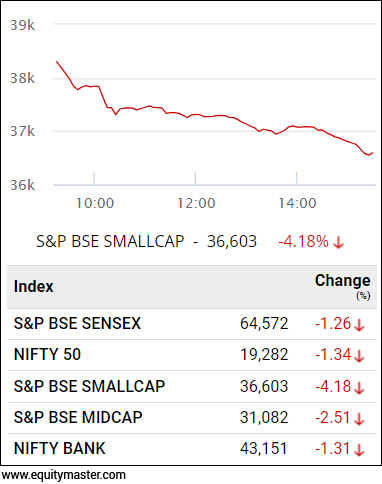

The benchmarks BSE Sensex and NSE Nifty saw a fall of over 1.3%, enough to get investors and traders panicking.

Broader markets were hammered to an even greater extent. Look at the chart of the BSE smallcap index in yesterday's trade.

To put things into context, the Indian share market has been falling for the past four sessions now. Some investors have already started to wonder whether we're entering a bear market.

When emotions run high, it's very hard to hold on to your investments. The general instinct is panic selling.

And that's when investors get so lost and confused that they forget to analyse the fundamental reasons behind the correction.

Currently, the Indian share market is falling due to rising US bond yields, uncertainty over the Israel-Hamas conflict and a resultant fall in global markets.

We at Equitymaster believe these are normal up and down moves of the market. The really serious declines begin only when the benchmark index falls at least 10%. That's not happened as yet!

And even if something like that does happen, such correction would create good buying opportunities in fundamentally strong stocks for the long term.

That brings us to smallcaps.

You see, smaller companies have greater growth opportunities compared to their larger counterparts. That's what makes them compelling enough over largecap or bluechip stocks.

For example, Reliance adding a couple of billion rupees to its bottom-line by launching a new product would barely move its stock price.

But a small-cap stock announcing its foray into emerging fields or getting a new drug approval is enough to make a serious impact in its stock price overnight.

It's not all rainbows for smallcaps either. Smallcap stocks are impacted more than their large counterparts during market drawdowns. But the silver lining is that during the rebound, they bounce back stronger.

Keeping that in mind and the current correction in smallcaps, let's look at the top 5 undervalued smallcap stocks that could possibly do well in 2024.

These companies are filtered using Equitymaster's powerful stock screener.

#1 VLS Finance

First on this list is VLS Finance.

Established in 1986, VLS Finance is a multi-faceted, multi-divisional, integrated financial services group.

It provides various services like asset management, strategic private equity investments, arbitrage, and investment banking.

What factors make VLS Finance undervalued at the current valuations?

At the current price, the stock trades at a single-digit price to earnings (PE) multiple of 3.4x. This compares with its long term 5-year average PE of 4.1x.

Even if we compare it on a price to book value basis, the stock trades at a P/BV multiple of 0.27x. It's like getting a 100 rupee note at Rs 27.

VLS Finance is a debt free company, able to generate positive net cash flow.

Although its financial performance was impacted in FY23, the company is hopeful of improving margins in the coming quarters.

It also pays consistent dividends and has averaged a dividend yield of over 1% for the last seven years.

Promoters of the company continue to remain bullish as they keep buying shares from the open market. The shareholding data shows that promoters have taken their stake up constantly for the past two quarters.

They even bought back shares at Rs 200 earlier this year in January 2023.

Given the stark difference in its actual book value and the current market price, the stock could bounce back in the coming months, depending on the performance it puts out for FY24.

#2 Sandesh

Next on this list is Sandesh.

Established in 1923, Sandesh is one of Gujarat's largest and most influential media houses.

The company initially started off as a Gujarati daily newspaper. It has subsequently forayed into various other branches of the media and entertainment industry including television channels, magazines, OOH, and digital media.

Coming to its valuations...

The stock currently trades at a PE multiple of 6.4x. This compares with its 5-year average PE of 6.8x.

On the book value front, it trades at a P/BV multiple of 0.7x compared to its 5-year average of 0.6x.

In the financial year 2023, the company reported healthy growth in topline as well as bottomline owing to growth in its advertisement segment.

Since the coming year is an election year, experts are of the view that the company's revenue could shoot up even more and the advertisement revenue could particularly get a boost.

You see, the media industry plays a crucial role in an election year as political parties interact with voters using print media, television, radio, etc. This translates into revenue growth for the media industry.

Sandesh, with its strong brand and established presence in Gujarat, could be one of the biggest beneficiaries.

Currently, the company has zero debt on its books and it has maintained a healthy liquidity position. The company's profits also show an increasing trend.

This could continue in the medium term and stock could possibly catch up to its book value.

#3 Gujarat State Fertilizers

Third on this list is Gujarat State Fertilizers.

Gujarat State Fertilizers & Chemicals (GSFC), a government entity, manufactures various fertilizers and industrial products like plastics & synthetic rubbers and man-made fibres.

The company's integrated manufacturing facilities enable it to benefit from synergies.

Fertilizers contribute around 70% to the company's operating income whereas industrial products contribute the balance.

The stock currently trades at a PE multiple of 7.4x. This compares with its 5-year average PE of 7.7x.

On the book value front, it trades at a P/BV multiple of 0.7x compared to its 5-year average of 0.5x.

Shares of the company got a boost in the past one month after the Israel-Hamas war impacted fertilizer prices, making GSFC a prime beneficiary of this trend.

The geopolitical conflict has raised concerns regarding the global supply chain of potash fertilizer.

Ashdod Port, which is a significant hub for Israel's potash fertilizer exports located north of Gaza, is now operating in an emergency mode due to the conflict. This situation might place around 3% of the global potash supply at risk.

What makes GSFC compelling apart from valuations is that its fertilizer segment has started to show improvement for the past couple of quarters.

The company also has a long history of paying dividends. In FY23, GSFC declared a one-time special dividend of 6.3%. This was significantly higher than the company's average dividend yield of 2.1% over the past 5 years.

It's also planning a massive capex for the next four years, around Rs 28 bn. This should keep the company in healthy stead going forward.

#4 HUDCO

Fourth on this list is HUDCO.

Housing & Urban Development Corporation (HUDCO) is a public limited company (Government of India undertaking).

Being majorly owned by the centre, the company receives support in terms of board representation and access to low-cost funds.

The company is primarily engaged in the business of financing housing and urban development activities in the country.

Over the years, HUDCO has played a significant role in the implementation of its various initiatives in urban infrastructure and social housing projects.

Coming to valuations, the stock currently trades at a PE multiple of 8.4x. This compares with its 5-year average PE of 5.3x.

On the book value front, it trades at a P/BV multiple of 0.9x compared to its 5-year average of 0.7x.

While this may seem like an overvaluation, a fundamentally strong stock available at single digit PE multiple and below 1x its book value might make the case.

The valuations have shot up a bit in recent months after the company announced fundraising plans this year. In March 2023, HUDCO's board announced plans to raise Rs 180 bn as part of its fundraising exercise.

The company is in the process of seeking fresh registration under the RBI as a housing finance company.

It also rewards shareholders consistently by making large dividend payouts. HUDCO boasts of a high dividend yield of 5.2% on its current market price.

Given the company's rising exposure to urban infrastructure, in line with the government's increased focus towards infrastructure development, it might set the stage for HUDCO, which sanctions loans under various infrastructure schemes.

Government holding in HUDCO stands at over 81% as on 30 June 2023.

#5 Ambika Cotton

Last on this list is Ambika Cotton.

The company manufactures premium quality compact and elitwist cotton yarn used in hosiery and weaving.

It is an established textile player in the international and domestic yarn market, with exports constituting over 60% of its revenues.

The stock currently trades at a PE multiple of 9.3x. This compares with its 5-year average PE of 8.8x.

On the book value front, it trades at a P/BV multiple of 1.1x compared to its 5-year average of 1.2x.

The undervaluation could be due to the fact that the Indian cotton textile industry has faced multiple challenges in the past one year. The high price volatility and the higher absolute raw materials prices have dented the margins.

The relative price differences compared to the international markets have led to a massive competitive disadvantage for most Indian textile players.

Apart from this, a demand slowdown due to geopolitical tensions and inflation in European and US economies has dented the profitability further.

The company also posted a decline in revenue for the first quarter of FY24 while operating margins declined mainly on account of higher inventory cost and increase in employee expenses.

Given its established market position and relatively strong balance sheet with zero debt, the company could possibly tide over this subdued phase.

The company also pays consistent and higher dividend every year.

Going forward, Ambika Cottom is well-poised to benefit from the growth in the textile segment, which comes from rising disposable income in the country and the low cost advantage in terms of skilled manpower.

Conclusion

It's said price is what you pay and value is what you get.

Going by this simple principle, one of the greatest investors of all time Warren Buffett has been able to beat the market for decades running.

Many companies fall out of favour due to whatsoever reasons, be it unexpected losses or growth in the business slowing down.

But once the business gets up and running and investors come back to their senses, the share price of these undervalued companies shoots back up to its intrinsic value.

The companies mentioned above are strong contenders to bounce back in the medium term.

To conclude, stay invested, wait for the recovery, and be greedy when others are fearful (that means right now.)

Happy Investing!

Safe Stocks to Ride India's Lithium Megatrend

Lithium is the new oil. It is the key component of electric batteries.

There is a huge demand for electric batteries coming from the EV industry, large data centres, telecom companies, railways, power grid companies, and many other places.

So, in the coming years and decades, we could possibly see a sharp rally in the stocks of electric battery making companies.

If you're an investor, then you simply cannot ignore this opportunity.

Details of our SEBI Research Analyst registration are mentioned on our website - www.equitymaster.comDisclaimer: This article is for information purposes only. It is not a stock recommendation and should not be treated as such. Learn more about our recommendation services here...

ABOUT EQUITYMASTER

Since 1996, Equitymaster has been the source for honest and credible opinions on investing in India. With solid research and in-depth analysis Equitymaster is dedicated towards making its readers- smarter, more confident and richer every day. Here's why hundreds of thousands of readers spread across more than 70 countries Trust Equitymaster.

PREMIUM PRODUCTS

QUICK LINKS

POPULAR TOPICS

- Multibagger Penny Stocks

- Basics of Value Investing

- Benjamin Graham

- How to Invest in Gold

- How to Invest in Silver

- Best Stocks to Buy Today

- Best Small-cap Stocks to Buy

- Best Bluechip Stocks to Buy

- Guide to Penny Stocks

- How to Invest in the Share Market

- Warren Buffett - The Value Investor

- Pick the Best Multibagger Stocks

TRENDING TOPICS

Donate to credible NGOs in the sector of your choice (ii) Claim 50% tax benefit u/s 80G (iii) Receive periodic reports.")

Copyright © Equitymaster Agora Research Private Limited.

Whitelist | Refer | Terms | Privacy | Contact | About | Sitemap

Equitymaster Agora Research Private Limited (Research Analyst)

SEBI (Research Analysts) Regulations 2014, Registration No. INH000000537.

103, Regent Chambers, Above Status Restaurant, Nariman Point, Mumbai - 400 021. India.

Telephone: +91-22-61434055. Email: info@equitymaster.com. Website: www.equitymaster.com.

CIN:U74999MH2007PTC175407

Name of the Compliance & Grievance Officer: Ms Sonal Ramachandran

Telephone: +91-22-61434003 | Email: compliance@equitymaster.com

LEGAL DISCLAIMER:

Investment in securities market are subject to market risks. Read all the related documents carefully before investing.

Registration granted by SEBI and certification from NISM in no way guarantee performance of the intermediary or provide any assurance of returns to investors.

All rights reserved. Any act of copying, reproducing or distributing this newsletter whether wholly or in part, for any purpose without the permission of Equitymaster is strictly prohibited and shall be deemed to be copyright infringement.

Equitymaster Agora Research Private Limited (Research Analyst) bearing Registration No. INH000000537 (hereinafter referred as 'Equitymaster') is an independent equity research Company. Equitymaster is not an Investment Adviser. Information herein should be regarded as a resource only and should be used at one's own risk. This is not an offer to sell or solicitation to buy any securities and Equitymaster will not be liable for any losses incurred or investment(s) made or decisions taken/or not taken based on the information provided herein. Information contained herein does not constitute investment advice or a personal recommendation or take into account the particular investment objectives, financial situations, or needs of individual subscribers. Before acting on any recommendation, subscribers should consider whether it is suitable for their particular circumstances and, if necessary, seek an independent professional advice. This is not directed for access or use by anyone in a country, especially, USA, Canada or the European Union countries, where such use or access is unlawful or which may subject Equitymaster or its affiliates to any registration or licensing requirement. All content and information is provided on an 'As Is' basis by Equitymaster. Information herein is believed to be reliable but Equitymaster does not warrant its completeness or accuracy and expressly disclaims all warranties and conditions of any kind, whether express or implied. Equitymaster may hold shares in the company/ies discussed herein. As a condition to accessing Equitymaster content and website, you agree to our Terms and Conditions of Use, available here. The performance data quoted represents past performance and does not guarantee future results.

Equitymaster requests your view! Post a comment on "Top 5 Undervalued Smallcap Stocks to Watch Out for in 2024". Click here!

Comments are moderated by Equitymaster, in accordance with the Terms of Use, and may not appear

on this article until they have been reviewed and deemed appropriate for posting.

In the meantime, you may want to share this article with your friends!